The Essential Guide to Special Needs Trusts: Protecting Your Child's Future (And Your Peace of Mind)

If you're the parent of a child with special needs, you've probably asked yourself this question a thousand times:

"What happens to my child when I'm gone?"

It's not morbid. It's not pessimistic. It's responsible.

Because the truth is: if you don't plan, your child could lose critical government benefits, face financial exploitation, or end up in the care of someone who doesn't understand their needs.

Special Needs Trusts solve this problem.

Today, I'm walking you through everything you need to know—what they are, how they work, how to fund them, and how to choose the right trustee.

This is for mothers, fathers, grandparents, and caregivers who refuse to leave their children's futures to chance.

I was fortunate enough to have spent the first nearly decade of my federal government career working for the Social Security Administration as a Title II Claims Representative (retirement, survivors, disability), and later as a Paralegal in the Office of Appellate Operations at headquarters in Woodlawn, Maryland. This was before I attended and graduated from law school, where I briefly practiced Juvenile and Special Education Law. I admit having an affinity towards the aged and those with disabling conditions, and my background offers a unique perspective on how to advocate for the rights of those oftentimes left behind.

What is a Special Needs Trust?

A Special Needs Trust (SNT), also called a Supplemental Needs Trust, is a legal arrangement that allows you to provide financial support to a disabled beneficiary without disqualifying them from government benefits such as Supplemental Security Income (SSI) or Medicaid.

Why Does This Matter?

Government benefits like SSI and Medicaid have strict asset and income limits:

SSI: An individual cannot have more than $2,000 in countable resources

Medicaid: Varies by state, but typically $2,000–$2,500 in assets

If your child inherits money directly (via a will, life insurance, or bank account):

They could lose SSI and Medicaid benefits

They'd have to "spend down" the inheritance to re-qualify

They might lose access to critical healthcare, housing assistance, and support services

A Special Needs Trust protects both the inheritance AND the benefits.

What Can a Special Needs Trust Pay For?

The trust can pay for supplemental needs—things that improve quality of life but aren't covered by government benefits:

✅ Education and training programs

✅ Medical and dental expenses not covered by Medicaid

✅ Rehabilitation services

✅ Recreational activities and hobbies

✅ Travel and vacations

✅ Personal care attendants (beyond what's covered)

✅ Electronics, computers, phones

✅ Home furnishings and modifications

✅ Entertainment (movies, concerts, sports events)

What it CANNOT pay for:

❌ Food

❌ Shelter (rent, mortgage, utilities)

❌ Cash directly to the beneficiary

These would reduce SSI benefits dollar-for-dollar.

Types of Special Needs Trusts

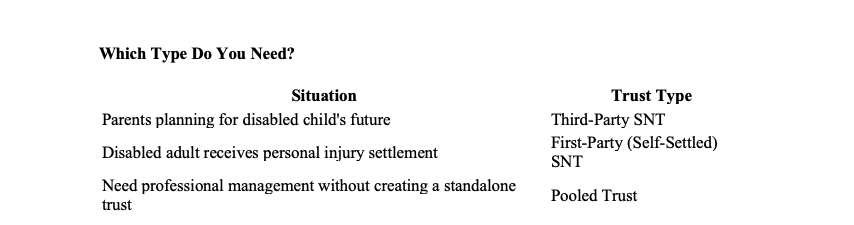

There are three main types of Special Needs Trusts:

1. Third-Party Special Needs Trust

Who creates it: Parents, grandparents, or other family members

Whose money funds it: The family's money (NOT the disabled person's assets)

When to use it:

Estate planning for parents of a disabled child

Receiving life insurance proceeds or inheritances on behalf of a disabled child

Key Feature: The trust creator controls the terms—who the trustee is, how funds are distributed, and what happens to remaining assets when the beneficiary dies.

Remaining Assets: Can go to siblings or other family members (not required to go to the state)

2. First-Party (Self-Settled) Special Needs Trust

Who creates it: The disabled person themselves (or their legal representative)

Whose money funds it: The disabled person's OWN assets (personal injury settlement, inheritance received directly, back pay from SSDI, etc.)

When to use it:

A disabled adult receives a personal injury settlement

A disabled person inherits money directly (and needs to protect government benefits)

Key Feature: Must be irrevocable and established before age 65

Remaining Assets: After the beneficiary dies, Medicaid gets reimbursed for benefits paid during the beneficiary's lifetime (called "Medicaid payback")

3. Pooled Trust

Who creates it: A nonprofit organization

Whose money funds it: The disabled person's assets (like a first-party trust, but managed collectively)

When to use it:

A disabled person has assets, but the family doesn't want to serve as trustee

Want professional management without high individual trust costs

Need immediate setup (faster than creating a standalone trust)

Key Feature: Disabled person's funds are "pooled" with other beneficiaries' funds for investment purposes, but each person has a separate account

Remaining Assets: Remaining funds typically stay in the pool to benefit other disabled beneficiaries (though some states allow a portion to go to family)

How to Fund a Special Needs Trust

Special Needs Trusts need funding to be useful. Here are the most common methods:

1. Life Insurance

How it works:

Parents take out a life insurance policy and name the Special Needs Trust as the beneficiary.

Why it's effective:

Provides a large, tax-free lump sum when parents die

Ensures the trust is funded even if parents haven't accumulated significant savings

Premiums are affordable (especially when purchased young and healthy)

Example:

A couple with a 10-year-old daughter with Down syndrome purchases a $500K life insurance policy. They name their Third-Party Special Needs Trust as the beneficiary. When they die, the trust receives $500K tax-free to care for their daughter for life.

🤞🏽 Pro Tip: Consider a second-to-die (survivorship) life insurance policy—it's cheaper than two individual policies and pays out when the second parent dies (when the child truly needs the funds).

2. Direct Contributions (During Life)

How it works:

Parents, grandparents, or other family members contribute money directly to the trust during their lifetime.

Why it's effective:

Allows the trust to grow over time

Can take advantage of compound interest

Provides flexibility to fund the trust gradually

Example:

Grandparents contribute $10,000/year to their grandson's Special Needs Trust as part of their estate planning strategy.

3. Inheritances and Bequests

How it works:

Family members name the Special Needs Trust as a beneficiary in their wills.

Why it's effective:

Ensures disabled person doesn't accidentally receive an inheritance directly (which would disqualify them from benefits)

Allows extended family to contribute

Critical: Make sure ALL family members (grandparents, aunts, uncles, siblings) know to leave inheritances TO THE TRUST, not directly to the disabled person. This is a big one because if they leave money to the special-needs child in their own wills, they can trigger the problem the trust seeks to avoid.

4. Retirement Accounts

How it works:

Parents name the Special Needs Trust as beneficiary of their 401(k), IRA, or other retirement accounts.

Tax Consideration:

Retirement accounts are subject to income tax when distributed. This is doable, but can be sticky. I highly advise you to consult a (good) tax advisor to structure distributions properly.

Choosing the Right Trustee

The trustee manages the Special Needs Trust and makes distribution decisions.

This is one of the most important decisions you'll make.

Qualities to Look For:

✅ Understanding of Special Needs: Knows your child's medical, emotional, and social needs

✅ Financial Competence: Can manage investments, pay bills, and file tax returns (🤞🏽make sure they have been properly filing their own!)

✅ Long-Term Commitment: Willing and able to serve for decades (your child's lifetime)

✅ Compassion and Advocacy: Will fight for your child's best interests

✅ Trustworthiness: Unquestionable integrity (they'll have access to significant assets)

Options for Trustees:

1. Family Member (Sibling, Aunt, Uncle, Cousin)

Pros:

Knows and loves your child

No fees (or nominal compensation)

Personal connection

Cons:

May lack financial expertise

Could face family conflict (especially if also a beneficiary)

May predecease your child or become unable to serve

Best for: Smaller trusts (<$250K), close-knit families, when a family member has financial literacy

2. Professional Trustee (Bank, Trust Company, Attorney)

Pros:

Expertise in trust administration and investments

Continuity (won't die or become incapacitated)

Neutral third party (avoids family conflict)

Cons:

Fees (typically 1–2% of trust assets annually)

May not know your child personally

Can feel impersonal

Best for: Larger trusts (>$500K), complex family situations, long trust durations

3. Co-Trustees (Family Member + Professional)

Pros:

Combines personal connection with professional expertise

Family member advocates for child's needs; professional handles finances

Checks and balances

Cons:

Potential for disagreement between co-trustees

More complex administration

Best for: Medium to large trusts, when you want both personal care and professional management

Special Consideration: Corporate Trustees vs. Individual Professional Trustees

Corporate Trustee (Bank/Trust Company):

Institutional continuity

Higher fees

Less personal

Individual Professional Trustee (Attorney, Financial Advisor):

Personal relationship

Lower fees

May retire or become unavailable

Common Mistakes to Avoid

Mistake #1: Not Creating a Special Needs Trust at All

Many parents assume their other children will "take care of" their disabled child informally.

Why this is risky:

No legal obligation for siblings to use inherited money for a disabled sibling

Disabled sibling could lose government benefits

Family conflict over money

No protection if sibling divorces, faces bankruptcy, or predeceases disabled sibling

Mistake #2: Leaving Money Directly to the Disabled Child

Even a small inheritance can disqualify a person from SSI and Medicaid.

Solution: ALWAYS leave money to the Special Needs Trust, not the disabled person directly.

Critical: Make sure ALL family members (grandparents, aunts, uncles) know this.

Mistake #3: Naming the Incorrect Beneficiary on Life Insurance

If you name your disabled child as the direct beneficiary on your life insurance policy, they'll receive the money outright—and lose government benefits.

Solution: Name the Special Needs Trust as the beneficiary, NOT the child.

Mistake #4: Not Funding the Trust

Creating a trust document is not enough—it must be funded. Period.

Solution: Fund with life insurance, direct contributions, or bequests in your will.

Mistake #5: Choosing an Improper Trustee

Choosing a trustee based on feelings ("my oldest child") rather than qualifications can backfire.

Solution: Choose based on financial competence, understanding of special needs, and long-term commitment. For Special Needs Trusts, you would be wise to strongly consider appointing a professional trustee or co-trustee.

How to Get Started

Step 1: Consult an Estate Planning Attorney

Special Needs Trusts are complex and must comply with federal and state laws. Work with an attorney experienced in special needs planning who can navigate these waters. Incorrect drafting of the trust in how it’s paid and protective verbiage to clarify when a trustee uses funds or if a spendthrift clause should be added can make or break the benefit of having a Special Needs Trust.

Step 2: Determine Funding Amount

Estimate how much your child will need over their lifetime:

Medical and therapy costs

Housing and personal care

Recreational and quality-of-life expenses

Use life insurance to bridge the gap between current savings and future needs.

Step 3: Choose a Trustee

Evaluate family members, professionals, or co-trustee arrangements. Discuss the role with candidates before naming them.

Step 4: Fund the Trust

Set up life insurance, direct contributions, or bequests in your will.

Step 5: Communicate with Family

Make sure ALL family members know:

The trust exists

They should leave inheritances to the trust (not directly to your child)

Who the trustee is and how to contact them

Step 6: Review Regularly

Review the trust every 3–5 years or after major life changes (divorce, the birth of additional children, or changes in the child's needs).

Special Needs Trusts & LegalShield

If you're setting up a Special Needs Trust, you'll need legal help.

LegalShield can assist with:

✅ Initial consultations about trust options

✅ Document reviews (trust agreements, beneficiary designations)

✅ Establish your trust or coordinate with your estate planning attorney

✅ Ongoing updates and modifications

Individual LegalShield plans start at $29.95/month.

📩 Want to explore LegalShield? Reply to this blog or email info@eastoceanstrategies.com.

📩 Want to explore LegalShield?

Reply to this blog or email info@eastoceanstrategies.com.

Conclusion: You Can't Do Everything—But You Can Do This

Raising a child with special needs is exhausting, overwhelming, and beautiful.

You can't control everything. But you can control this:

✅ Ensuring your child is financially secure when you're gone

✅ Protecting their government benefits

✅ Choosing a trustee who will advocate for them

✅ Providing for their quality of life

A Special Needs Trust is your gift of security, dignity, and love.

Don't wait. Life happens. Start today.

Additional resources…