Financial Independence for Women: 3 Protection Strategies You Can't Afford to Skip

Financial independence for women isn't just about earning more or saving more.

It's about protecting what you've built—your income, your assets, your family, and your legacy.

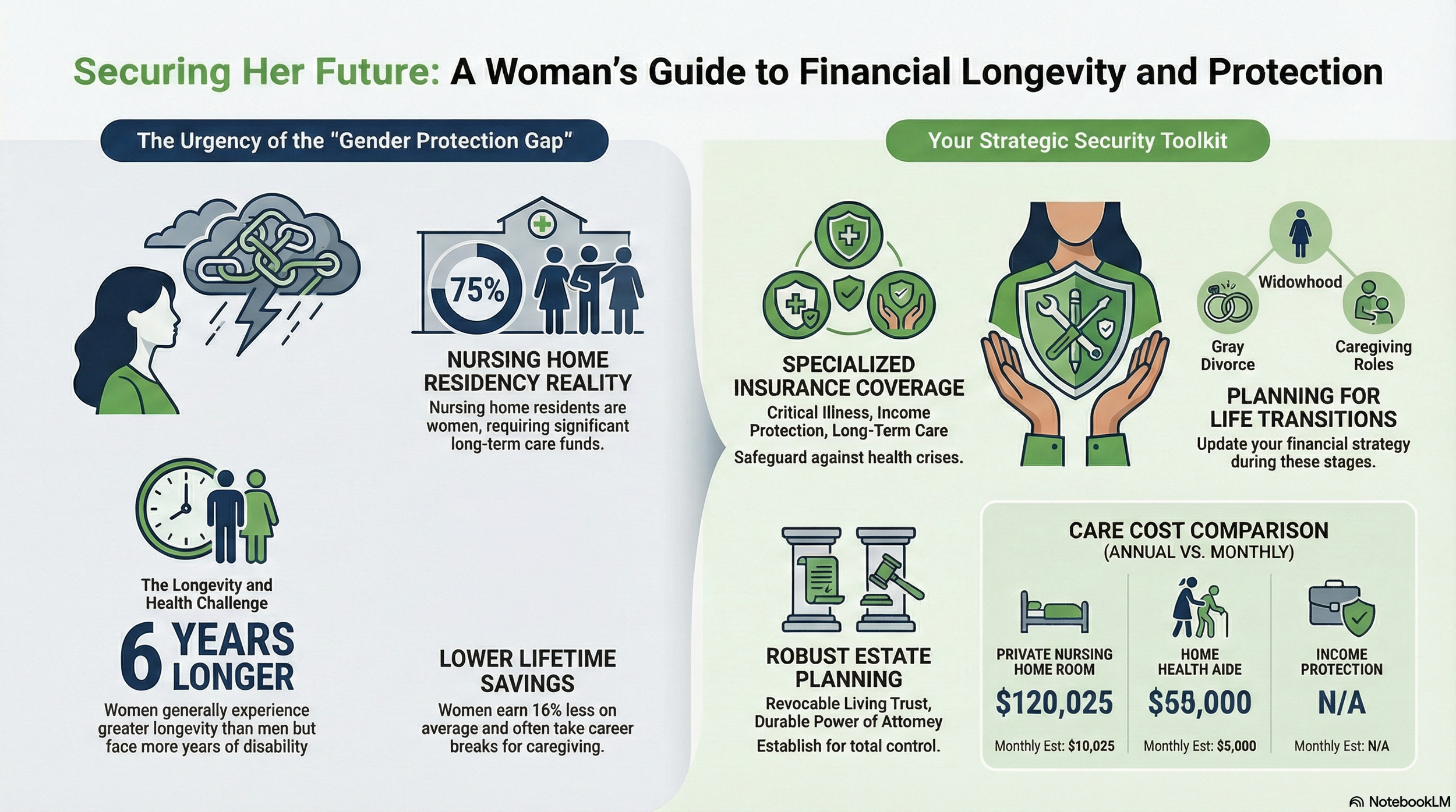

Here's the truth: Women face unique financial challenges that men don't.

💰 Longer lifespans (women live 5–7 years longer than men on average)

💰 Lower lifetime earnings (due to wage gaps and career interruptions)

💰 Greater caregiving burden (for children, aging parents, or both)

💰 Higher healthcare costs in retirement

Yet, women are consistently underinsured—especially when it comes to life insurance, disability coverage, and estate planning.

This Women's History Month, let's change that.

There’s the math.

Here are 3 protection strategies every woman needs to build true financial independence.

Strategy #1: Life Insurance – Women Need MORE, Not Less

The Myth:

"Life insurance is for breadwinners. Since I don't earn as much (or I'm a stay-at-home mom), I don't need as much coverage."

The Reality:

Women need just as much—if not more—life insurance than men.

Here's why:

1. Unpaid Labor Has Massive Economic Value

If you're a stay-at-home parent or primary caregiver, your labor has economic value—even if you're not drawing a paycheck.

Replacing your contributions would cost:

Childcare: $15,000–$30,000/year

Housekeeping: $10,000–$20,000/year

Meal prep and planning: $5,000+/year

Transportation and logistics: $5,000+/year

Financial and household management: Priceless

If you died tomorrow, who would do this work? Your spouse would need to hire help—or quit their job.

Life insurance coverage recommendation: $250K–$500K minimum, even if you're not the primary earner.

2. Women Live Longer—So Surviving Spouses Need More

Women outlive men by an average of 5–7 years. If your husband dies first, you'll need financial resources to:

Cover living expenses for those extra years

Pay for long-term care (which women are more likely to need)

Maintain your standard of living

Life insurance on your spouse protects you. Make sure his coverage is adequate for your long-term needs.

3. Single Mothers Carry Disproportionate Burdens

If you're a single mother, you are the sole financial provider AND caregiver. If something happens to you:

Who raises your children?

Who pays the mortgage?

Who funds their education?

Life insurance is non-negotiable. It ensures your children are financially cared for, even if you're not there.

Coverage recommendation: at least 10x your annual income.

Case Study: Meet Nicole Carter

Background:

49 years old, healthcare administrator, Raleigh, NC

Divorced, two college-age kids (20 and 22)

Caring for her aging mother (76) part-time

Annual income: ~$105K

The Problem:

Nicole is the financial anchor for three generations—her kids, herself, and her mother. If she died or became disabled, everyone would suffer.

The Solution:

We helped Nicole secure:

1. Whole Life Insurance ($300K)

Provides a death benefit for her kids

Includes living benefits she can access if diagnosed with a critical or terminal illness (useful for long-term care needs)

Builds cash value she can borrow against if needed

Premium: ~$250/month

2. Disability Insurance ($5,000/month benefit)

Replaces 60% of her income if she can't work

Elimination period: 90 days

Benefit period: To age 65

Premium: ~$140/month

3. LegalShield Select Plan ($20.95/month)

Will preparation and updates

Power of attorney and healthcare directive assistance

Elder care legal consultations for her mother

Divorce-related document reviews (post-decree modifications)

Total Monthly Investment: ~$411/month

Peace of Mind: Priceless.

Key Takeaway:

Life insurance isn't a luxury—it's a cornerstone of financial independence for women.

📲 Get a personalized life insurance quote: Book a free consultation

Strategy #2: Estate Planning – Don't Leave Your Legacy to Chance

The Myth:

"I don't have enough assets to need estate planning."

The Reality:

Estate planning isn't about wealth—it's about control.

If you die without a will or estate plan:

The state decides who inherits your assets

The court appoints a guardian for your minor children

Your family faces costly probate proceedings

Your healthcare wishes may be ignored

Women—especially single women, divorced women, and mothers—need estate planning documents.

The 8 Essential Estate Planning Documents

Sidebar: You can get additional insight from an earlier blog we posted at the top of 2026 - The Fresh Start Financial Protection Plan: 3 Essentials to Lock Down in 2026

Personal Documents:

Last Will and Testament – Directs asset distribution and names guardians for minor children

Advance Healthcare Directive / Living Will – Specifies medical care wishes if you're incapacitated

Financial Power of Attorney – Designates someone to manage finances if you can't

HIPAA Authorization – Allows access to your medical records

Durable Power of Attorney – Broader authority for legal and financial matters

Guardian Appointment – Names who will care for your minor or disabled children

Pet Placement Designation – Ensures your pets are cared for

Anatomical Gift Declaration – Documents organ donation wishes

Where to Get Them:

Free from your doctor's office, hospital, or AARP

Affordable fillable bundles with all 8 available at EastOceanStrategies.com/shop

All LegalShield plans provide for a will, an advanced directive, and a power-of-attorney document

Work with an estate planning attorney for complex situations

Special Considerations for Women

Single Women:

Without a spouse, you need to explicitly designate who will:

Make medical decisions for you

Manage your finances if you're incapacitated

Inherit your assets

Don't assume your parents or siblings will automatically have legal authority—put it in writing.

Divorced Women:

After divorce, update:

Beneficiaries on life insurance, retirement accounts, and bank accounts

Your will and power of attorney documents

Healthcare directives

Guardian appointments for children (if applicable)

Do NOT leave your ex-spouse as a beneficiary unless intentional.

Mothers (Married or Single):

Name a guardian for your minor children in writing

Consider a trust to manage assets for your children until they're adults

Designate a trustee to manage the trust (can be the same person as the guardian, or different)

Key Takeaway:

Estate planning protects your family and ensures your wishes are honored—no matter what.

📥 Download our free estate planning checklist: Get your checklist

Strategy #3: Disability Insurance – Protect Your Income-Earning Ability

The Myth:

"I have savings. I'll be fine if I can't work for a while."

The Reality:

Savings run out. Disability insurance ensures you're covered for months—or years—if you can't work.

Why Women Need Disability Insurance

1. Women Experience Disabilities at Similar Rates to Men

1 in 4 workers will become disabled before retirement (Social Security Administration). Illness and injury don't discriminate by gender.

2. Women Have Fewer Financial Cushions

Due to wage gaps and caregiving responsibilities, women typically have:

Lower lifetime earnings

Smaller emergency funds

Less retirement savings

If you lose your income, you have less runway before a financial crisis.

3. Women Are More Likely to Be Caregivers

If you're caring for children, aging parents, or both—and you become disabled—who takes care of them? Disability insurance ensures you can still support your dependents even when you can't work.

How Disability Insurance Works

What It Covers:

Replaces a portion of your income (typically 60%) if you're unable to work due to illness or injury.

Key Features:

Elimination Period: Waiting period before benefits start (30, 60, 90, or 180 days)

Benefit Period: How long benefits are paid (2 years, 5 years, to age 65)

Own Occupation vs. Any Occupation: "Own occupation" pays if you can't do YOUR job; "any occupation" pays only if you can't do ANY job

Cost:

For a healthy 40-year-old woman earning $75K/year:

Monthly benefit: ~$3,750 (60% of income)

Premium: ~$120–$180/month

Nicole's Disability Insurance (Case Study Continued)

Nicole's disability insurance provides:

$5,000/month benefit (60% of her $105K income)

90-day elimination period (she uses savings + accident insurance to cover the first 3 months)

Benefits to age 65 (long-term protection)

If Nicole becomes disabled, she can still:

Pay her mortgage

Support her kids through college

Cover her mother's care expenses

Maintain her standard of living

Without disability insurance? Nicole would drain her savings in 6 months and potentially lose everything she's worked for.

Key Takeaway:

Your income is your most valuable asset. Protect it.

📲 Get a disability insurance quote: Book a free consultation

BONUS: Legal Protection for Women (LegalShield)

Women navigate unique legal challenges:

Divorce and custody matters

Elder care legal issues

Estate planning for blended families

Business contracts for side hustles

Identity theft (women are disproportionately targeted)

LegalShield provides:

✅ Will and power of attorney preparation

✅ Divorce consultation and document review

✅ Elder care legal guidance

✅ Contract reviews

✅ Identity theft restoration services

✅ 24/7 emergency legal access

Plans start at $29.95/month.

📲 Learn more about LegalShield: Contact us

Conclusion: Financial Independence = Financial Protection

Financial independence isn't just about what you earn or save.

It's about protecting your ability to earn, securing your family's future, and ensuring your wishes are honored.

This Women's History Month, commit to:

✅ Getting adequate life insurance

✅ Creating or updating your estate plan

✅ Protecting your income with disability insurance

✅ Adding legal protection with LegalShield

You've worked too hard to leave your future to chance.

Let's build your protection plan together.